“The supranational sovereignty of world bankers is surely preferable to the national auto-determination practiced in past centuries.”

David Rockefeller

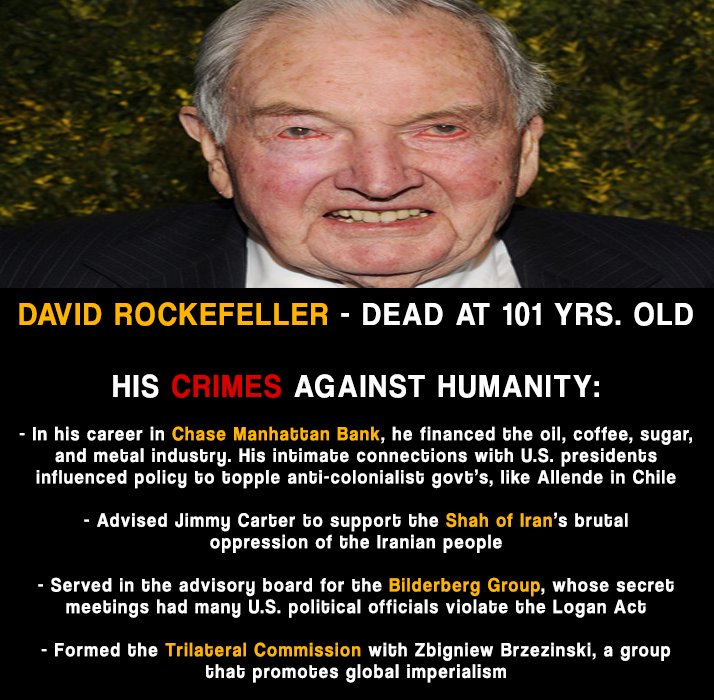

We say it isn’t!!!

A spectre haunts the entire world – including our own nation. This is the spectre of ever-growing debt and loss of national sovereignty to international banks and the plutocracy of “world bankers” – the ‘1%’’ that seek to impose a new form of monetary debt feudalism. The result is harsh cuts in private incomes and/or public spending, widespread child, food and fuel poverty, unemployment, homelessness and loss of vital public services such as medical care - not to mention global ecological devastation, wars and death. The spectre can be compared to a global economic pandemic. This pandemic however, is not the sort caused by a nasty bug or virus. Instead it is the result of a totally unquestioned but highly toxic belief.

This belief is shared by politician and parties of left, centre and right and alike - indeed even by the far left and far right. It is also perpetuated by the governments, press and media of all nations – who have turned it into nothing less than a global ‘Big Lie’ - one that both the leaders and peoples of most nations, including our own, often swallow even without even knowing it.

The belief, though never even questioned in parliament, press or news media is a very simple one: namely that governments are dependent either on taxation or on borrowing from private banks and financial markets to fund public spending and promote economic growth.

This belief is not only held by parties and politicians who prefer to reduce taxes and public spending, and seek to impose ever harsher ‘austerity measures’ to cut the national deficit. It is also shared by politicians and parties who prefer to ‘tax and spend’ and want their government to borrow more in order to maintain or increase public spending and promote economic growth.

The paradox here is that it is precisely public borrowing from the private finance sector that makes economic growth more important than it would otherwise be – for it is needed mainly just to provide the means to pay off ever-growing amounts of private, corporate and national debt and compound interest.

“In a time of deceit, telling the truth is a revolutionary act.”

George Orwell

The truth that now needs to be told is that no nation or state, ruler or government ever needs to borrow any money from private banks or moneylenders. Instead, as Lincoln recognised – and proved so successfully in practice - it just needs to create and issue its own money:

“The Government should create, issue, and circulate all the currency, and credits needed to satisfy the spending power of the Government, and the buying power of consumers.”

We need a ‘New Economics Movement’ to re-affirm this basic economic truth.

Paradoxically however, the truth itself is far from being ‘new’. It was recognised by the Spartans, by the ancient Greeks and their philosophers. It was recognised by the Roman Empire and its Caesars – who successfully poured their own state currency into the lands they conquered to stimulate ‘economic growth’. The policy of creating and issuing their own currency was followed by the Byzantine and Holy Roman Emperors.

It was also followed by most English monarchs since the 12th century – or was so until the Free Coinage Act of 1666, which took away the sovereign prerogative of the monarch to issue and create money, and the subsequent planning and founding of a privately owned ‘Bank of England’ – against the opposition of both the landowning Tories and leading economists such as David Ricardo.

This historic change - one that was to have global significance - was symbolised by deliberately burying the type of currency issued by British monarchs for hundreds of years - so-called ‘tally sticks’ – under the new temple-like building that still constitutes the Bank of England. The Bank of England was built like a temple because it was a temple - a temple to a new god and a new monotheistic religion – not a religion that believed in a divinely appointed monarch but one whose sole god was the god of money – ‘the monotheism of money’.

“The Bank was to be allowed to create bank notes in an amount equal to the money it lent to the government. This is another way of saying it could use government debt as its reserves or collateral. For example: the Crown wants a loan from the Bank; the Bank has no money of its own but creates money for the loan out of thin air, based on the reserve assets of the Crown’s resulting debt to it.” Stephen Zarlenga, The Lost Science of Money

The economist David Ricardo immediately saw what scam the new ‘Bank of England’ represented.

“Suppose that a million of money should be required to fit out an expedition. If the state issued a million of paper … the expedition would be fitted out without any charge to the people; but if a [private] bank issued a million of paper, and lent it to the government at 7%, … the country would be charged with a continual tax of 70,000 per annum.”

Instead of this Ricardo proposed a establishing an English National Bank capable of issuing its own money without borrowing from private banks and bankers. Similarly, the centralisation of credit in the hands of the state was one of the central planks of Marx’s ‘Communist Manifesto’. Yet neither Ricardo nor Marx were alone among political and parliamentary opponents of the Bank of England. In fact many Tories, monarchists, economists, politicians and thinkers of all hues would have agreed with the following remarks of Marx, which complement those of Ricardo:

“At their birth the great banks, decorated with national titles, were only associations of private speculators, who placed themselves by the side of governments, and thanks to the privileges they received, were in a position to advance money to the state … The Bank of England begin with lending money to the government at 8%; at the same time it was empowered by Parliament to coin money out of the same capital, by lending it again to the public in the form of bank notes … It was not long before this credit money, made by the Bank itself, became the coin in which the Bank of England made its loans to the state, and paid, on account of the state, the interest on the public debt. It was not enough that the Bank gave with one hand and took back more with the other; it remained, even whilst receiving, the eternal creditor of the nation down to the last shilling advanced.”

“The public debt becomes one of the most powerful levers of primitive accumulation [of capital]. As with the stroke of an enchanter’s wand, it endows barren money with the power of breeding and this turns into capital, without the necessity of exposing itself to the troubles and risks inseparable from its employment in industry … The state creditors actually give nothing away, for the sum lent is transformed into public bonds, easily negotiable, which go on functioning in their hands just as hard cash would.”

Here Marx also echoes Aristotle, who argued that whilst commodities such as corn or cattle could naturally breed more of themselves and in this way provided the basis for a type of natural ‘interest’ payment when lent out (at least until corporations such as Monsanto came to place global patents on farmer’s seeds or breeds of livestock) the breeding of money through usury and interest was wholly un-natural.

THE COLONISTS REBEL

“The refusal of King George to allow the colonies to operate an honest money system which freed the ordinary man from the clutches of the money manipulators was probably the prime cause of the revolution.” Benjamin Franklin, Founding Father

The surrender of the sovereignty of individuals and nations – whether to the power of monarchs or to ‘money power’ - was resisted only in America. That is why, as Benjamin Franklin recognised, monarchs and money power united to attack the rebel colonists and undermine by all means possible the issuing of paper currencies such as the 'Continental' and ‘Greenback’, particularly if issued as legal tender, i.e. as money in itself and not an IOU or promise to pay the holder in the form of silver or gold. Eventually this monetary rebellion was brought to heel by the private bankers barons – who eventually succeeded in making it redeemable with gold that had then to be borrowed from them at interest! Yet until this point, even British parliamentarians had had occasion to see how the American colonists lived far better lives - through issuing their own debt- and interest-free money - than the miserably impoverished masses in a Britain ruled by the money power of private bankers.

And today, nations worldwide - whether monarchies, democracies or dictatorships - have surrendered their most basic sovereign right – the right to issue and create their own interest-free money. Instead they have made themselves dependent on borrowing – at interest – from commercial international banks and a global banking mafia - ‘the 1%. Yet how is the belief - the global big lie - that governments need to borrow from private banks still sustained? It is sustained by phrases such as ‘money doesn’t grow on trees’, by repeated negative references to governments ‘printing money’ – or by dire warnings that if they did the result would be hyperinflation. All of this is nonsense. It is based on the seemingly common sense idea that you can’t just ‘make money from nothing’. And yet that is precisely what private and international banks and financial speculators do today. Banks do not lend from capital reserves or savings. They literally lend money into existence from nothing – just by keying in figures into borrower’s electronic accounts. That fictional loan money, created by a few keystrokes, then counts as the banks ‘assets’, and the loans themselves (however ‘bad’ or ‘toxic’) are free to be sold on – making yet more money for the banks in addition to the interest gained on them.

In simple terms, the very act of taking out a loan - whether on the part of an individual, business or government – actually gives private banks permission not only to create the money that they lend from nothing but also claim it as their own money - even though they didn’t have it before! To top it all, the banks then demand that the borrower pay them ‘back’ this money that they didn’t have but created from nothing – but this time with compound interest payments charged on top! This is nothing but legalised counterfeiting – not through forgery of paper money– but by just creating money electronically through keystrokes on a computer. It is also legalised fraud – for the borrower doesn’t know that in taking out a loan he is allowing the bank not just to make its own money from nothing – without labouring for it – but to make far more money for itself than it lends out – none of which benefits the borrower. Morally, therefore, it is not borrowers but the banks themselves that should be charged interest on the money they lend into existence, i.e. create without having to engage in any form of genuinely productive work. As for the old but still-repeated tale that ‘money doesn’t grow on trees’, whilst this may apply to ordinary households it certainly does not apply to nations or to privately owned banks. For one thing private banking is a financial ‘tree’ – ‘making money from nothing’ and from its ‘negative money’ - from want of money and debt.

MAKING MONEY FROM NOTHING

As William Paterson, one of the key founders of the Bank of England admitted:

“The bank hath benefit of interest on all moneys which it creates out of nothing.”

This basic truth has been confessed countless times by bankers themselves:

“The modern banking system manufactures money out of nothing. The process is perhaps the most astounding piece of sleight of hand that was ever invented.”

Josiah Stamp, ex-governor of the Bank of England,

“I am afraid the ordinary citizen will not like to be told that the banks can and do create money. And they who control the credit of the nation direct the policy of Governments and hold in the hollow of their hand the destiny of the people.”

Reginald McKenna, as Chairman of the Midland Bank, addressing stockholders in 1924

“The banks do create money. They have been doing it for a long time, but they didn’t realise it, and they did not admit it. Very few did. You will find it in all sorts of documents, financial textbooks, etc. But in the intervening years, and we must be perfectly frank about these things, there has been a development of thought, until today I doubt very much whether you would get many prominent bankers to attempt to deny that banks create it.”

H.W. White, Chairman of the Associated Banks of New Zealand

“Banks lend by creating credit. They create the means of payment out of nothing.”

Ralph M. Hawtry, former Secretary to the Treasury

“Commercial banks create checkbook money whenever they grant a loan, simply by adding new deposit dollars in accounts on their books in exchange for a borrower’s IOU.” The Federal Reserve Bank of New York

“This is a staggering thought. We are completely dependent on the Commercial Banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the Banks create ample synthetic money, we are prosperous; if not, we starve. We are, absolutely, without a permanent money system. When one gets a complete grasp of the picture, the tragic absurdity of our hopeless position is almost incredible, but there it is. It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse, unless it becomes widely understood, and the defects remedied very soon.”

Robert H. Hemphill, Federal Reserve Bank, Atlanta, Georgia

Congressman Patman: "How did you get the money to buy those 2 billion dollars’ worth of Government securities in 1933?” Governor Eccles: “We created it.” Patman: “Out of what?” Eccles: “Out of the right to issue credit money.” Patman: “And there is nothing behind it, is there, except our Government’s credit?” Eccles: “That is what our money system is. If there were no debts in our money system, there wouldn’t be any money.”

Dialogue notated during hearings of the House Committee on Banking and Currency, September 30, 1941. ‘Governor’ Eccles was Chairman of the Federal Reserve Bank.

THE FOUNDATIONAL PRINCIPAL OF A NEW ECONOMICS

If national governments – not private banks – reasserted their sovereign right to create and issue money of their own for public spending there would not only be no need for them to borrow from private bankers – there would also be no need for them to tax the people. The whole battle between economic policies based on ‘tax and spend’ policies and those which seek to cut both taxation and public spending would become totally meaningless – as it would be already if the real issue were understood. This is the issue of who has the power to create, issue and regulate a nation’s money supply – private bankers or the nation state. Today it is private bankers who have this power, and it is this that results (as it did in the past) in inflation, economic depression and cuts in public spending.

For all these reasons the principal policy and demand of a New Economics Movement must be that the power of money creation be restored to the nation and state. For in this way alone can true economic sovereignty be restored to all nations - with money used for the benefit of the people and not the banks and financial markets. In this way also the pressure to maintain economic growth at a rate that everyone knows is fast depleting the planet’s resources will be reduced – because no element of that growth will any longer be needed simply as a source of taxation to pay back or bailout the big banks. Their power rests on the simple reality that today it is not paper or cash but electronic money - created as debt - that accounts for 97% of the nation’s money supply – and therefore actually depends on debt to sustain that supply. In such a debt-based monetary system, if all debt to the banks were paid off, both the banks and the nation would be bankrupt. A no-win situation unless money creation itself is re-nationalised and thereby also control of the nation’s money supply.

“Whoever controls the volume of money in our country is absolute master of all industry and commerce … and when you realize that the entire system is very easily controlled by a few powerful men at the top, you will not have to be told how periods of inflation and depression originate.”

James A. Garfield, assassinated President of the United States

“Issue of currency should be lodged with the government and be protected from domination by Wall Street. We are opposed to … provisions [which] would place our currency and credit system in private hands.”

Theodore Roosevelt

“The bankers own the world. Take it away from them, but leave them the power to create money and control over that money, and they will create that money right back again. Take this power away from bankers and all great fortunes will disappear, and they ought to disappear, for this then would be a happier, better world to live in … But if you want to continue to be slaves to the banker and pay the cost of your own enslavement, then let the bankers continue to create money and control credit.”

Josiah Stamp

The dangers associated with the total control over the money supply of the nation by privately owned commercial banks was long ago recognised by Ricardo, who advocated instead both a truly public or National Bank and the creation of special monetary commissioners to determine how much new money it could create and inject into the economy - thereby achieving far greater control of inflation than a totally unregulated and uncontrolled monetary system run for the benefit of private banks and financial speculators, or even the regulation of interest rates by today’s Bank of England – which allows the banks themselves to borrow at zero or even negative interest - whilst lending it out at any interest rate they choose.

Though the Bank of England was nationalised in 1946, its role as a central bank is now reduced to regulating monetary policy, and it can create money only through trading in government bonds (debts) or by borrowing and accumulating debt. At the start of the First World War however, a Currency and Bank Notes Act was passed which granted temporary powers to the Treasury in Great Britain for directly issuing banknotes to the value of £1 and 10/- (ten shillings) in the UK. These treasury notes had full legal tender status and were not convertible for gold through the Bank of England, thus replacing the gold coin in circulation to prevent a run on sterling and to enable raw material purchases for armament production. The wording on each note was:

UNITED KINGDOM OF GREAT BRITAIN AND IRELAND — Currency notes are Legal Tender for the payment of any amount — Issued by the Lords Commissioners of His Majesty's Treasury under the Authority of Act of Parliament (4 & 5 Geo. V c.14).

Treasury notes were issued until 1928, when the Currency and Bank Notes Act 1928 returned note-issuing powers to the banks. Today the Bank of England is still responsible for printing paper money and coins - which it can sell to commercial banks and thus use as a source of income. Yet this form of money now constitutes only 3% of the nation’s money supply - the remaining 97% being created from nothing by commercial banks. Significantly, Treasury notes were not redeemable in gold. This reflected another basic truth central to the New Economics Movement – namely that to serve as legal tender money need have token value with no intrinsic value in itself. Even if coins are made of gold or silver their value as money is completely distinct from their value as commodities in the form of precious metals – for monetary value can be decided by the state (by ‘fiat’). It was the attempt to base the value of money on precious metals such as gold and silver that led the Spartans to create their own form of fiat money from ‘base metals’ – using iron rendered valueless for any purpose – just as it led the English monarchs to use wood in the form of tally sticks.

CREATING DEBT-FREE MONEY THROUGH NEW NATIONAL CURRENCIES

In the face of the nationwide poverty, wage- and debt-slavery currently being imposed by the international banks in both the U.K., the U.S. and many countries of the Eurozone, - exemplified by the dramatic increase in unemployment, homelessness, child poverty and ‘food banks’ - the New Economics Movement proposes a radical strategy to counter ‘austerity terrorism’. At the heart of this strategy will be ‘free money’ i.e. the free distribution of a new debt- and interest-free national currency in any quantity and denominations, both in the form of paper money notes and as an electronic money system. The free money will be given firstly to independent local traders and then directly to people on the street and on their doorsteps. Distributing free money will itself constitute a high-profile and highly original form of electoral campaigning for fundamental monetary reform – one which is not based exclusively on distributing flyers or pamphlets, or just talking to people without anything more than words to give them. It will also be a way of directly demonstrating and modelling the very aims of this campaign for public money - by building a fully public ‘National People’s Bank’ from the ground up. This New Economic strategy could be implemented in three stages:

1. Creating a central website through which (a) anyone can download pre-designed images of and print any quantity of the new paper currency in different denominations (b) which explains the principle of its use and distribution (see below) and (c) that can also be used to log and track its distribution and circulation and form the basis of an electronic account, electronic currency and free ‘free-money’ cards.

2. Offering local independent traders and craftsmen – in particular independent food retailers such as bakers, butchers and grocers – any amount of the free money they wish. The sole condition imposed on receivers of the new currency will be a pledge (see below and printed on each note along with the address of the central website) to accept as payment from customers as much of the free currency as they ask to be given. Traders will also be encouraged to offer a part of this freely received money to their suppliers on the same conditions – thus establishing a supply chain and leading to a stage at which they pay their suppliers in the new currency.

3. Handing out the ‘new money’ freely on the high street or door-to-door, along with a list of local shopkeepers, traders and craftsmen and service providers willing to accept it.

It is important to emphasise three basic principles governing the new currency, namely that:

(1) the holder pledges to accept in payment for their own good or services as much of the new money they hold or use as payment for the goods and services of others

(2) the new currency will be a form of money in itself – a mere token of value with no intrinsic value. Thus whilst, for the purpose of domestic or international trade, the new currency will be purchaseable in Pounds or other currencies it will not be redeemable in those currencies i.e. holders of the new currency will not be able to exchange it for the official national currency or other currencies.

(3) the new public currency will be a truly national one – and not merely some form of local currency or LETS scheme, for example in the case of the Republic of the Isles, a ‘People’s Pound’.

Given the nature of the new currency, each note will therefore carry the following words:

If used in payment for goods or services from others, the holder promises to accept the amount on this note as payment for any goods or services of their own.

Each note will also carry a statement declaring that it can be bought with the official national currency or with foreign currencies but cannot be sold in exchange for them.

No comments:

Post a Comment